Between 74 and 89 per cent of retail forex traders lose money every quarter, by the brokers' own disclosed numbers under ESMA rules. The retail press blames the trader. From the desk, the answer is structural. The retail FX broker is engineered, end to end, to convert deposits into broker P&L. This note is the pro-side decomposition of that engine, drawn from FX Traders vs Brokers (Djellal Djouad, 2026).

1. A-book, B-book, hybrid: what comparison sites get wrong

Retail literature reduces broker types to an ethical choice. The reality is different. Pure A-book routes every order to an external liquidity provider. Pure B-book is the counterparty: when the client loses, the broker pockets the loss algebraically. The actual industry standard is hybrid: the broker scores each client in real time (deposit size, win rate, holding time, leverage). Profitable accounts are A-booked. Unprofitable accounts are B-booked. The classification is dynamic and undisclosed.

2. The five friction layers retail does not see

The retail debate fixates on the displayed spread. It is the least determining variable in actual P&L. The five layers: (1) visible spread bid-ask; (2) slippage asymmetric between displayed and applied price; (3) requote where the broker rejects and reproposes the worst of the two; (4) last look, a 50 to 200 ms window where the LP reviews price before accepting; (5) gap on session open or post-news, where retail stops do not trigger at displayed levels. Combined cost of layers 2 to 5 exceeds the visible spread by three to five times on a one-month measure.

3. The funnel: how a $500 deposit funds $200 of intermediation

Lifetime Value of a retail small account is 2.2 to 4.1 times the initial deposit. That LTV funds an acquisition envelope of $200 to $1,500 per client paid to a five-tier pyramid: Introducing Broker, affiliate, trainer rebated by broker, signal provider, copy-trading or PAMM platform. Each tier extracts in the deposit-to-loss path. The trader depositing $500 has already paid $150 to $300 in distributed intermediation before placing a single trade.

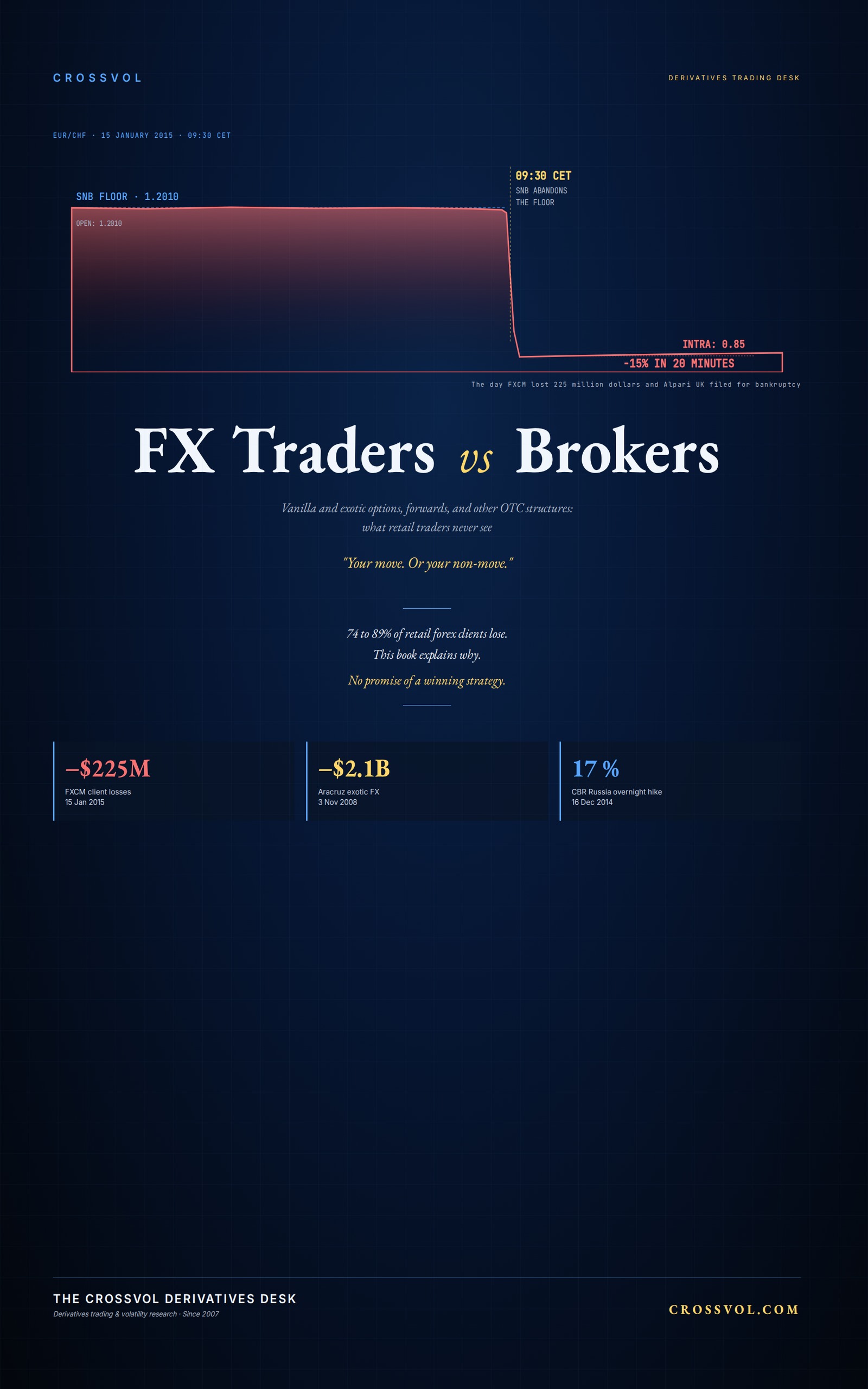

4. The case law: six precedents defining the operational space

FXCM Inc, 22 February 2017: CFTC settlement on the Effex Capital arrangement, $7M fine, US retail divestiture, CEO Dror Niv and MD William Ahdout personally banned. Alpari UK, 19 January 2015: special administration post-SNB, 70,000 active clients, £100M segregated, FCA mechanism preserved funds. Direct motivation for ESMA negative balance protection. ESMA, 27 March 2018: leverage caps 30:1 majors / 20:1 minors / 5:1 equities / 2:1 crypto; negative balance protection mandatory; 50% margin close-out; ban on monetary incentives; standardized risk warning displaying quarterly losing client percentage. MyForexFunds, 29 August 2023: 135,000 clients, $310M fees collected, no funded trader executed on a real market, conditions artificially degraded, payout thresholds retroactively cancelled.

5. Why retail directional spot FX produces bagholders in series

The dominant product is leveraged directional spot on a major pair, 20x to 100x, intraday horizon, technical signals and retail news. The pro sees option flow by strike and maturity, top-tier dealer runs, aggregated CFTC positioning, Bloomberg IB chats with ten sales in parallel, voice access to block-trading desks. Retail observes the statistical shadow of institutional decisions without accessing the mechanisms producing it. The pro observes the price and the flows that produced it simultaneously. Same game, broadcast through glass walls, five-second delay, half the cards missing.

6. The book

Full text covers 33 chapters: A-book / B-book mechanics, the funnel, last look, FXCM / Alpari / MyForexFunds case law, prop-firm hidden B-book, news trading, options-based macro discipline, structural exits from the glass room. Seven first-person desk chronicles. Annexes A to E. 57,189 words. The pro-side audit retail FX brokers do not want you to read.

This note summarises material from FX Traders vs Brokers (Djellal Djouad, 2026, CrossVol Research). It is not investment advice. ORCID: 0009-0002-4911-1118.